It was Monday morning. Not just any Monday, but the kind that determines whether the rest of the week will be controlled or chaotic. Ana, a financial controller at a payments fintech, arrived early at the office. Her coffee was still warm when she opened the main dashboard. At first glance, everything looked fine: millions of transactions processed over the weekend, active merchants, satisfied users. But it only took a few seconds to notice what no one wanted to see. The numbers didn’t match.

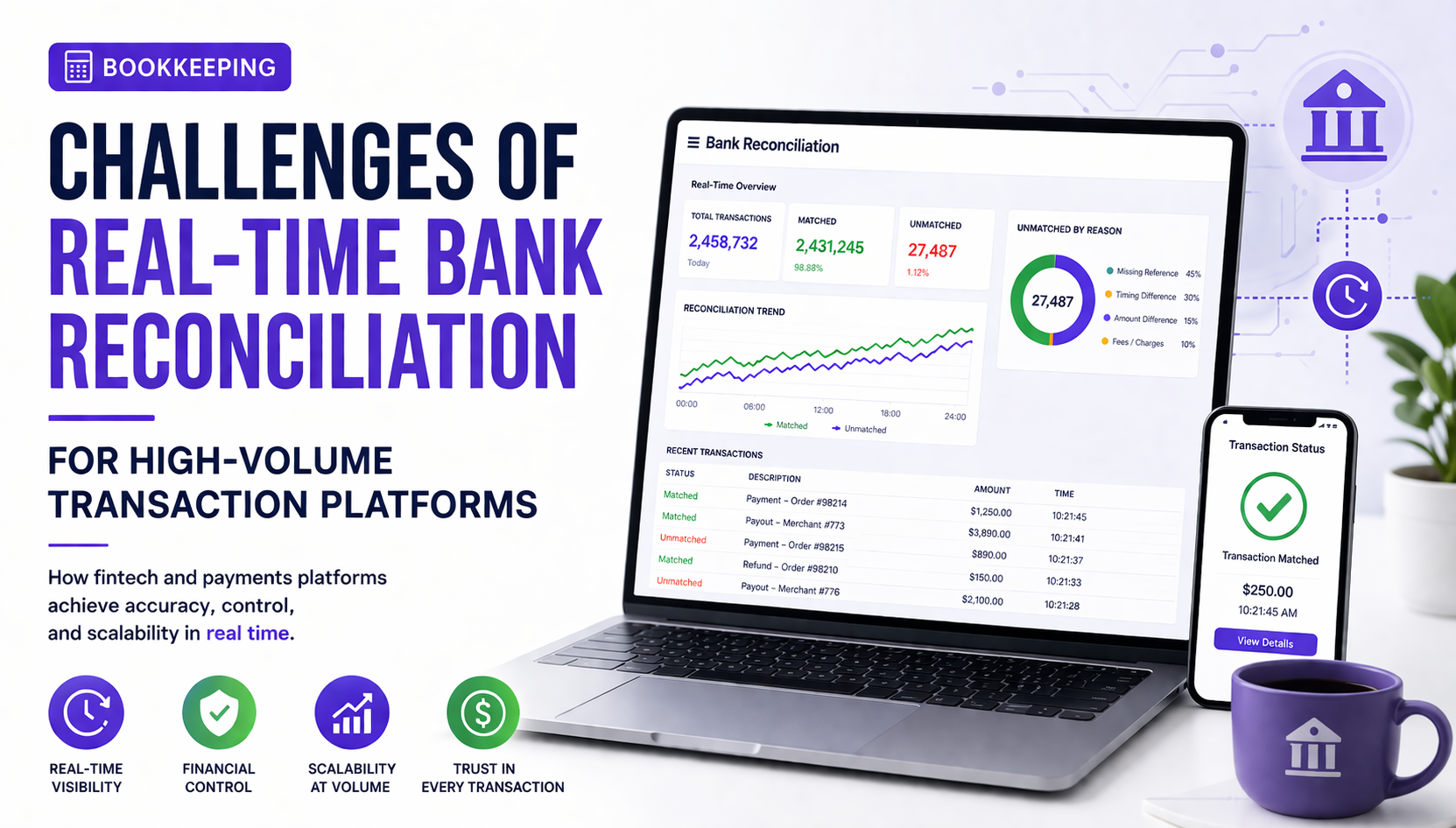

“We have a 3.2 million difference between our internal ledger and the bank,” she said without looking up. The silence in the room was expected. It wasn’t the first time. In high-volume transaction platforms, bank reconciliation stops being just an accounting task and becomes a critical operational control point. Every discrepancy represents time, money, and, most importantly, trust.

For years, bank reconciliation followed a retrospective logic. First, transactions were executed, then bank statements were received, and finally, records were compared. This model worked in low-volume environments, but in today’s fintech ecosystem, where thousands or even millions of transactions are processed per hour, this approach becomes obsolete. The gap between what happens on the platform and what the bank reflects creates friction that escalates quickly.

Ana and her team faced this reality every day. Duplicate transactions, payments without clear references, mismatches in settlement timing, fees applied out of sync. Each issue on its own was manageable. But together, multiplied by volume, they became a structural problem. It was no longer just about fixing errors, but about recognizing that the system itself needed to evolve.

That’s when they made a key decision: stop reconciling the past and start reconciling in real time. This shift didn’t simply mean speeding up existing processes; it required a complete redesign of the financial logic behind their operations. Real-time reconciliation demands that each transaction be validated almost at the exact moment it occurs, connecting internal systems with banking infrastructure continuously.

However, the first major obstacle appeared quickly. The traditional financial system is not designed to operate in real time. While fintech platforms can process payments in seconds, banks often rely on batch processes, cut-off windows, and settlement delays that introduce unavoidable latency. This asynchrony creates constant tension between the expectation of immediacy and operational reality.

Ana understood they couldn’t force the banking system to change, but they could adapt their internal model. Instead of seeking exact real-time matches, they began working with transaction states. Each transaction moved through stages, from pending to confirmed and finally settled. This allowed them to build a dynamic reconciliation model, one that evolves alongside the transaction rather than waiting for a final outcome.

As they progressed, another major challenge emerged: imperfect matching. In theory, reconciliation is about matching records. In practice, data rarely aligns perfectly. References may be incomplete, formats vary between systems, and timestamps don’t always match. This inconsistency caused traditional reconciliation methods to fail repeatedly.

To address this, the team implemented more flexible and intelligent rules. They introduced probabilistic matching mechanisms, strengthened the use of unique identifiers, and established configurable tolerance thresholds. They even incorporated models that learned from historical patterns to improve accuracy over time. Still, exceptions always existed, reminding them that full automation remains a work in progress.

The next challenge was scalability. As the fintech grew, transaction volume increased exponentially. What worked with hundreds of thousands of transactions began to break at millions. Processing times increased, systems became overloaded, and errors accumulated. At that point, the team realized that reconciliation needed to be not only accurate but also scalable.

The solution involved migrating to more robust architectures based on event-driven processing. Each transaction became an event that could be handled independently, allowing for greater flexibility and resilience. This approach didn’t eliminate errors, but it prevented isolated issues from affecting the entire system.

One of the most significant breakthroughs, however, was not technical but visual. Previously, when a discrepancy occurred, identifying its source was a long and frustrating process. There was no clear way to determine whether the issue originated from the bank, the payment gateway, or the internal system. The lack of visibility turned every error into a complex investigation.

To solve this, they developed real-time monitoring tools that allowed them to trace the full lifecycle of each transaction. Suddenly, problems were no longer invisible. Every discrepancy had a clear origin, a defined state, and a path to resolution. This level of traceability transformed how the team handled incidents.

As the operation matured, so did regulatory requirements. Auditors were no longer satisfied with end-of-day reconciliation. They demanded continuous evidence, automated controls, and the ability to trace any transaction at any moment. Real-time reconciliation shifted from being a competitive advantage to becoming an operational necessity.

Six months after that chaotic Monday, another similar morning arrived. Ana opened the dashboard again. This time, the numbers matched. But that wasn’t the most important part. What truly mattered was that if something stopped matching, the system would detect it within seconds. Uncertainty had been replaced with control.

Real-time bank reconciliation doesn’t eliminate challenges, but it fundamentally changes how they are addressed. It transforms reactive processes into dynamic ones, reduces reliance on manual intervention, and enables operations to scale without losing visibility. In the fintech world, where speed and accuracy are critical, this capability becomes a key differentiator.

In the end, Ana’s story isn’t just about bank reconciliation. It’s about adaptation. It’s about understanding that traditional processes cannot sustain modern business models. And it’s about recognizing that in a high-volume transaction environment, the real value lies not just in processing payments, but in having complete control over them.